2 minute read / Sep 2, 2021 /

Benchmarking Amplitude's S-1: How 7 Key Metrics Stack Up

Amplitude, a leading provider of web analytics, filed their S-1 earlier this week. The company leverages novel storage techniques to scalably collect data on how users engage with mobile apps and web sites. Amplitude counts Cisco, Adidas, PayPal and CapitalOne amongst its customers.

Amplitude offers three key products: analytics for measuring user behavior, experiment for testing new user flows, and recommendation which optimizes content for different user segments.

| Metric | 2019 | 2020 |

|---|---|---|

| Revenue, $M | 68.4 | 102 |

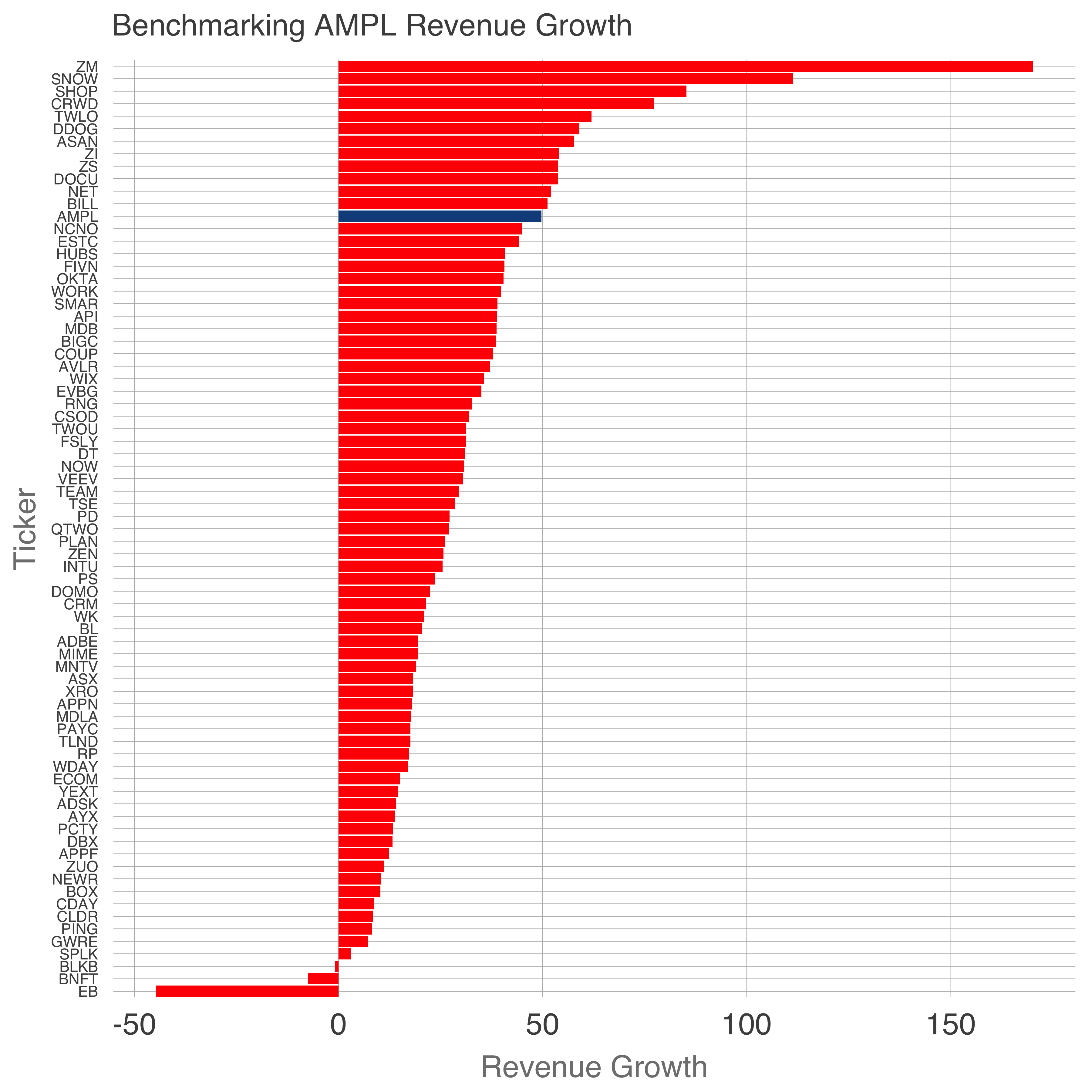

| Revenue Growth | - | 49.7% |

| Gross Margin | 67.7% | 70.0% |

| Sales Efficiency | - | 0.54 |

| Net Income Margin | -49.0% | -24.0% |

| Cash Flow from Operations Margin | -23.4% | -10.1% |

| Net Dollar Retention | 116% | 119% |

| Average Customer Value, $k | 92.6 | 98.6 |

| Customer Count | 739 | 1039 |

| Large Customer Contribution | 71% | 72% |

Amplitude’s revenue growth rate is in the top quartile for modern software companies at 49%.

The summary statistics of the business reveal a company with a fairly high contract value of $98,600 and the largest customers generating 72% of revenue, putting the business squarely in the enterprise segment of SaaS companies. Both the ACV and large customer contribution are increasing with time suggesting the company continues to focus up-market.

Amplitude has demonstrated improving efficiency characteristics across three key areas. The first is sales efficiency. The company spent $47m in 2019 on sales and marketing, and $52m in 2020, an increase of $3m or 6%, while growing revenues 49%. The 2020 sales efficiency is 0.54. Assuming current trends hold, sales efficiency in 2021 should nudge up to about 0.57.

Impressively, Amplitude has charted an increasing growth rate in the first half of the year. Comparing the first half of 2021 to the first half of 2020, the company grew 57%, eight percentage points higher than the annual figures. This while improving profitability and cash flow margins.

Similarly, net income margin (profitability) has increased from -49% to -24%. Cash flow from operations margin parallels the pattern, improving from -23% to -10%.

Where will Amplitude trade? I prepared a linear regression model using the top two correlated factors to enterprise value to forward revenue multiple (EV/Fwd Rev). The model predicts the company will trade at 22x forward, implying an enterprise value in the range of $5.8 - $6.2B.

Following the model of Asana, Slack, Spotify and others, Amplitude will conduct a direct listing on the day of their IPO. Congratulations to the entire Amplitude team on having built an impressive business and importantly the first publicly traded analytics company since Omniture debuted in 2006.