4 minute read / Mar 6, 2020 /

What I Expect in the Next Few Months in Startupland

I was on a panel yesterday to speak about the impacts of the coronavirus on financial markets and startups. Later in the afternoon, I read the Sequoia black swan memo. So I figured today, I’ll summarize my outlook on the next few months.

Startup Growth Rates

For startups, things will likely slow down. Longer sales cycles will be the leading indicator. At least, that’s my key metric for startup health over the next few months.

With travel curtailed, closing new customers will require selling over the phone/video - and it’s a bit harder to build trust, particularly for big deals over the phone. Bookings will be more volatile than in the past as a result. So, more pipeline is necessary to create consistency.

However, there’s a confounding factor: pipeline generation will be harder. Teams will be working from home. Consequently, we are all adapting to new working patterns. Additionally, organizers are canceling conferences. Inevitably, event lead generation will decline. Marketing teams and BDRs will need to rely on other channels and will saturate them. Everyone will do this at the same time, increasing CPCs/CPMs/CPAs and flooding email inboxes with marketing materials. Response rates will fall.

Startups should prepare a more conservative financial plan that delays non-essential hiring, conserves cash, and prepares the business. Equally important is creating a set of leading indicators that, once triggered, the business shifts to the conservative plan.

Some executive teams may prefer to move immediately to the conservative plan. Others may prefer to wait until they trip those key leading indicators: slower sales cycles and weaker lead generation. It depends on the business. In particular, the size of the balance sheet and the urgency to the buyer.

Fundraising

Fundraising velocity will likely slow from the fast pace we’ve seen for the same reasons as slowing sales: it’s just a bit harder to meet people.

Valuations may be pressured for companies raising capital now with more conservative growth plans. If startups project slower growth trajectories, then valuations will fall because the growth rates are the highest correlate of valuation multiples.

Also, the volatility in the stock market may pressure valuations, particularly in the growth stage. But as I wrote about earlier this week, the valuation multiples haven’t moved materially. We’re still close to all time highs, so this might be a bit more muted than one would expect.

Bullwhip Effect

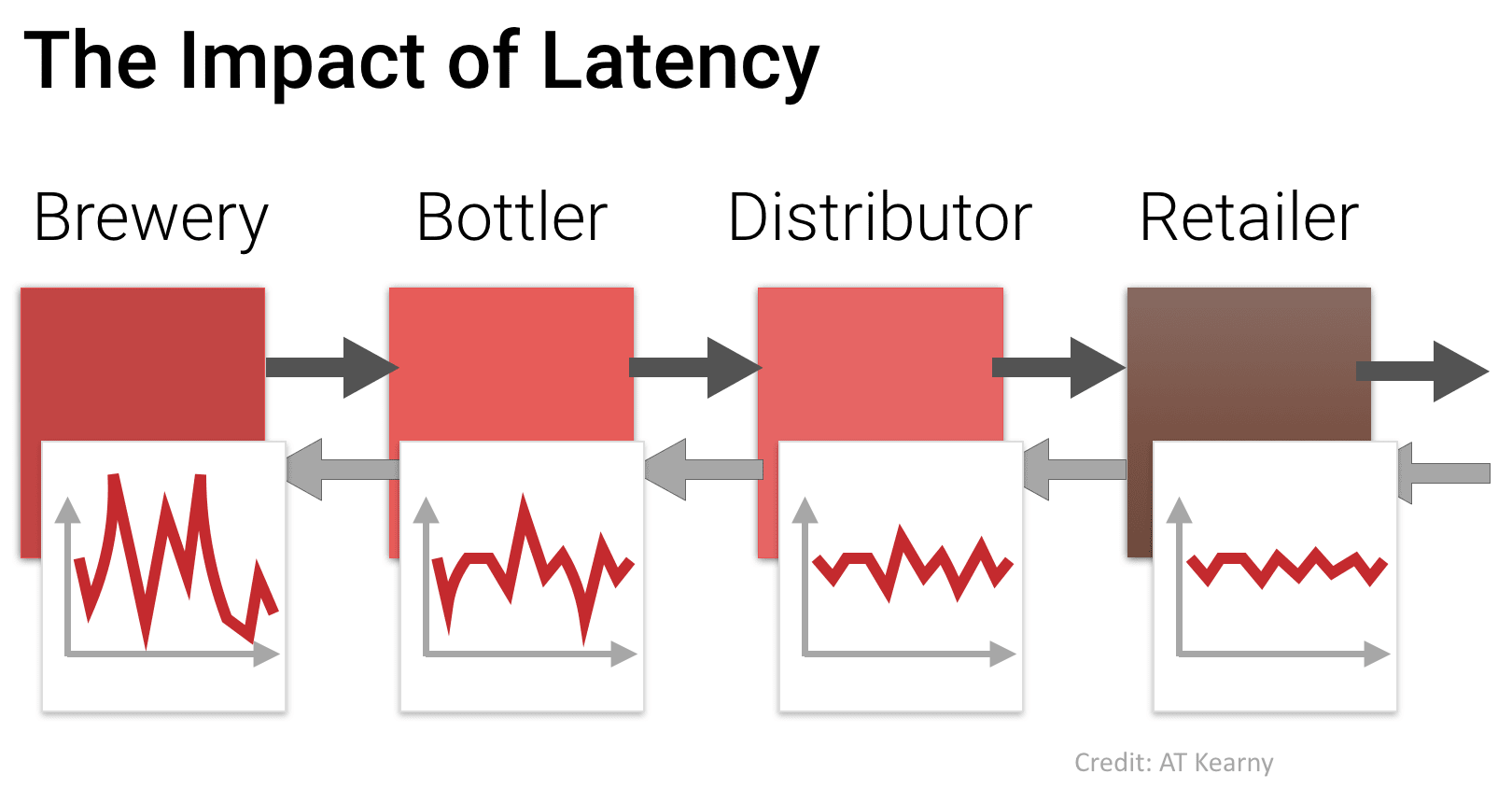

More broadly, I suspect many parts of the economy (and startups) will suffer from the Bullwhip Effect. The idea originates from MIT. I describe it in depth here and I’m pasting an image below.

The idea is that small changes in retail demand amplify into big swings up the supply chain. In this case, it’s a beer supply chain. The small perturbations in retail demand create a whip-like effect upstream. The brewer’s orders whipsaw up and down as retailers and the rest over-order and then under-order.

This will happen in many different industries. The net result is unpredictability. The volatility is going to sow doubt in investors’ minds. That will slow investment and lower valuations in public markets.

Monetary Policy

I interpret the Fed’s recent 0.5% rate cut as a way to maintain consumer confidence and maintain consumer spending to smooth out demand variance. Consumer confidence is important because consumer spending is driving most of the projected growth in GDP in the US in 2020.

With a projected 0.2% monthly increase straightlined for the rest of 2020, that implies about a 2.4% GDP growth. Before the coronavirus, the Fed was already projecting GDP growth of less than 2.0%, so consumer spending is critical.

As a counterpoint, business spending was soft at the end of last year and this uncertainty won’t help. So we should expect lower GDP in the US than we’re projecting. This will again pressure the public markets.

Outlook Ultimately, the more we can smooth any shocks and discontinuities, the better the overall economy will be because we won’t be subject to as great of a whip effect. The challenge is that each business will act independently. They may reduce their spending in small ways that cumulatively engender large swings.

I’m hopeful that the volatility we’re seeing today will subside quickly. For this quarter, it’s prudent to construct a more conservative plan and establish those leading indicators that trigger a switch to it.