1 minute read / Oct 13, 2022 /

How Low Could Valuations Go?

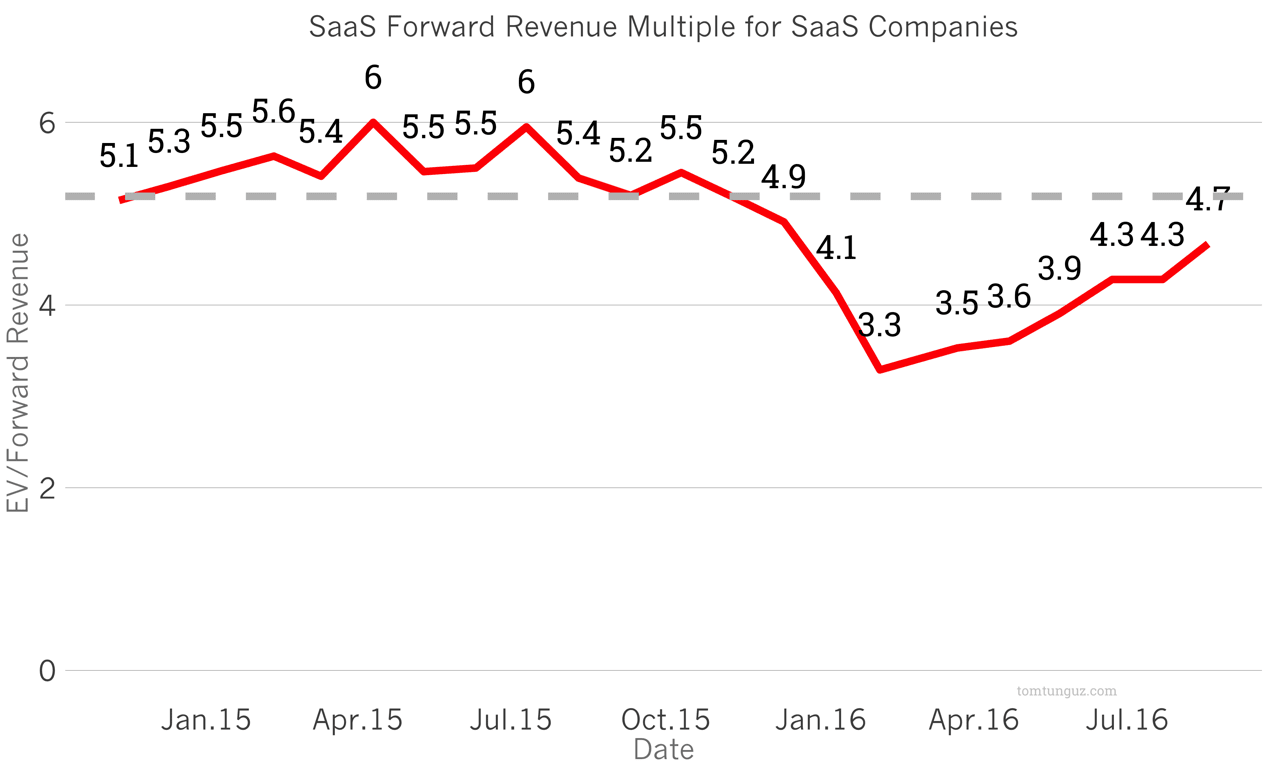

The public software market continues to compress. Enterprise-value-to-forward-revenue multiples are now below 2016 levels for the first time in 6 in years.

The 25th percentile of companies trade at 3.3x today compared to 4.0x in 2016. The median or 50th percentile trade at 4.9x vs 5.6x. The 75th percentile have resisted the downward pull & retain their premium: 7.3x vs 5.8x.

The Federal Reserve Bank raising rates has been a strong depressor of valuations. The rates on the 10 year bond correlate at -0.49 R^2, meaning yield changes explain about half of the forward multiple’s movement since 2019.

With the Fed seems intent on raising rates further, how low could forward multiples fall? A basic linear regression using this data produces this table

| 10 Year Rate | Implied Forward Revenue Multiple |

|---|---|

| 4.00% | 5.1x |

| 4.25% | 4.4x |

| 4.50% | 3.6x |

| 4.75% | 2.8x |

| 5.00% | 2.1x |

The linear model is quite sensitive to the increase in rates. It doesn’t consider any other factors & it’s R^2 is only about 0.5. But it does illustrate the impact of rates on software valuations.

Would it be crazy to see 3.3x forward? Not really. It happened in Feburary 2016.