2 minute read / Jun 27, 2018 /

A Deeper Dive into the Dynamics of the Seed Market

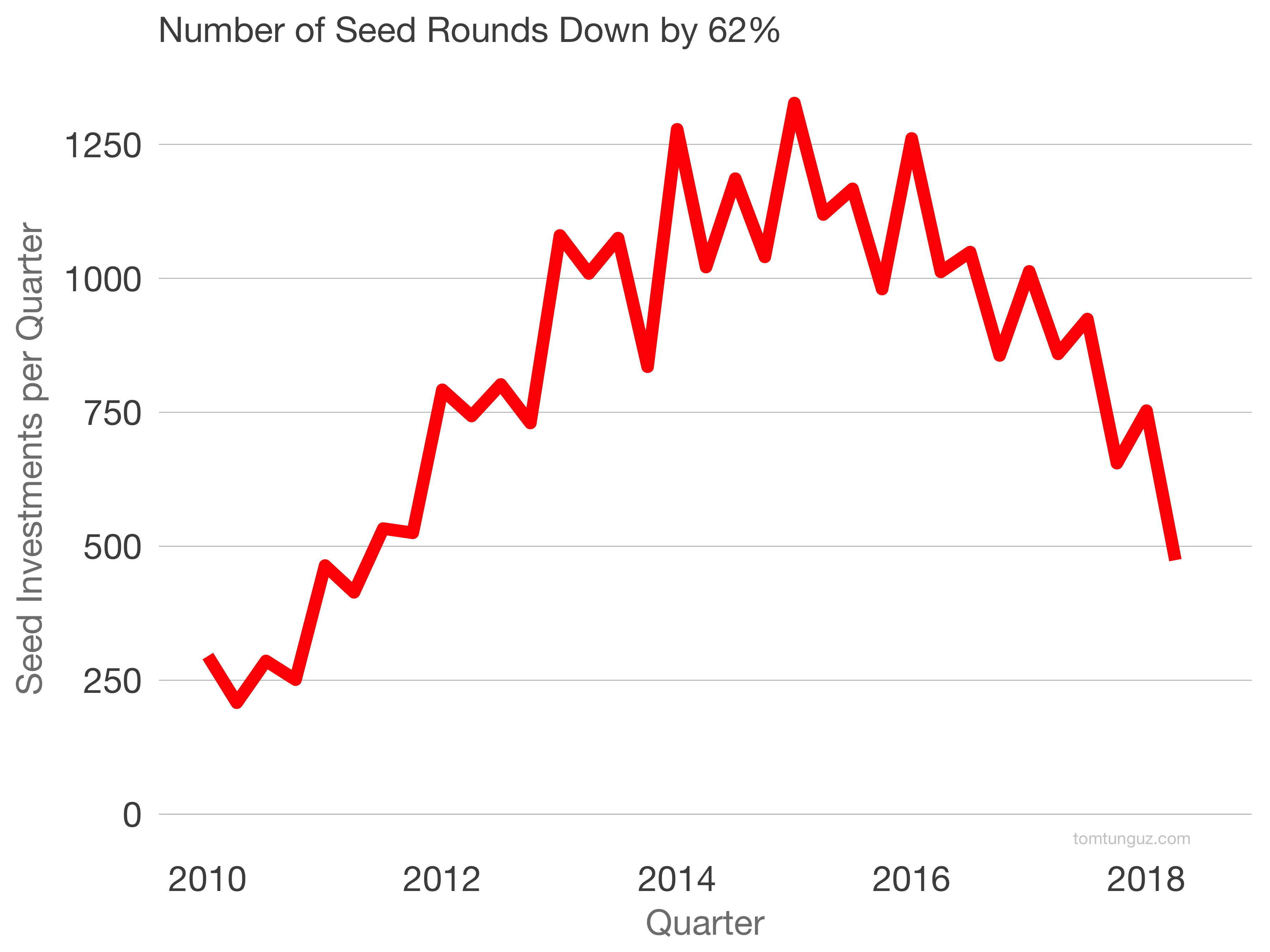

Earlier this week, I wrote about the collapse in the number of seed investments. I received many questions about the data, all the same. Why is this happening? This is a deeper dive into the data.

Earlier this week, I wrote about the collapse in the number of seed investments. I received many questions about the data, all the same. Why is this happening? This is a deeper dive into the data.

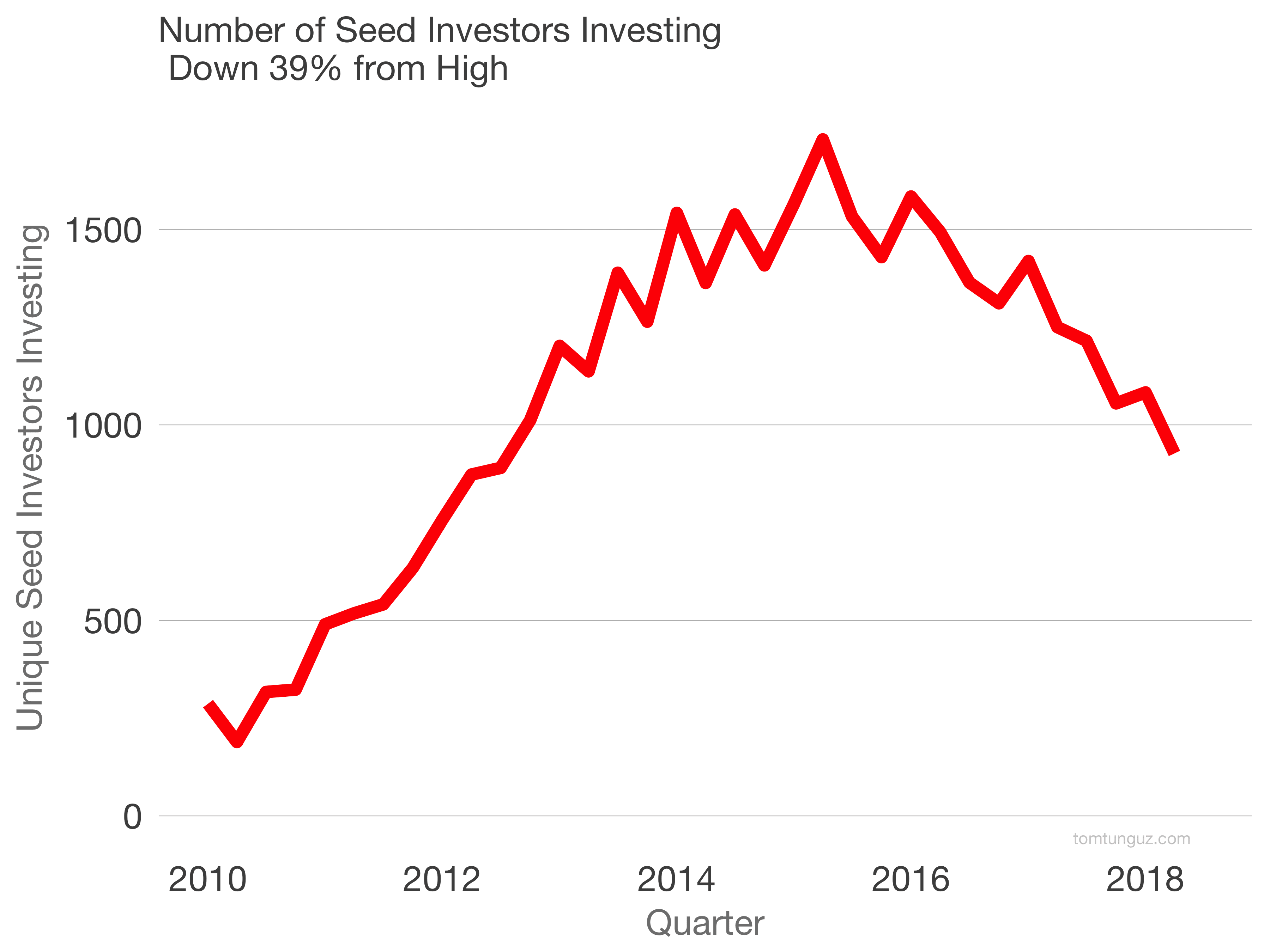

First, there are fewer seed investors participating in the market than in 2015, about 40% fewer.

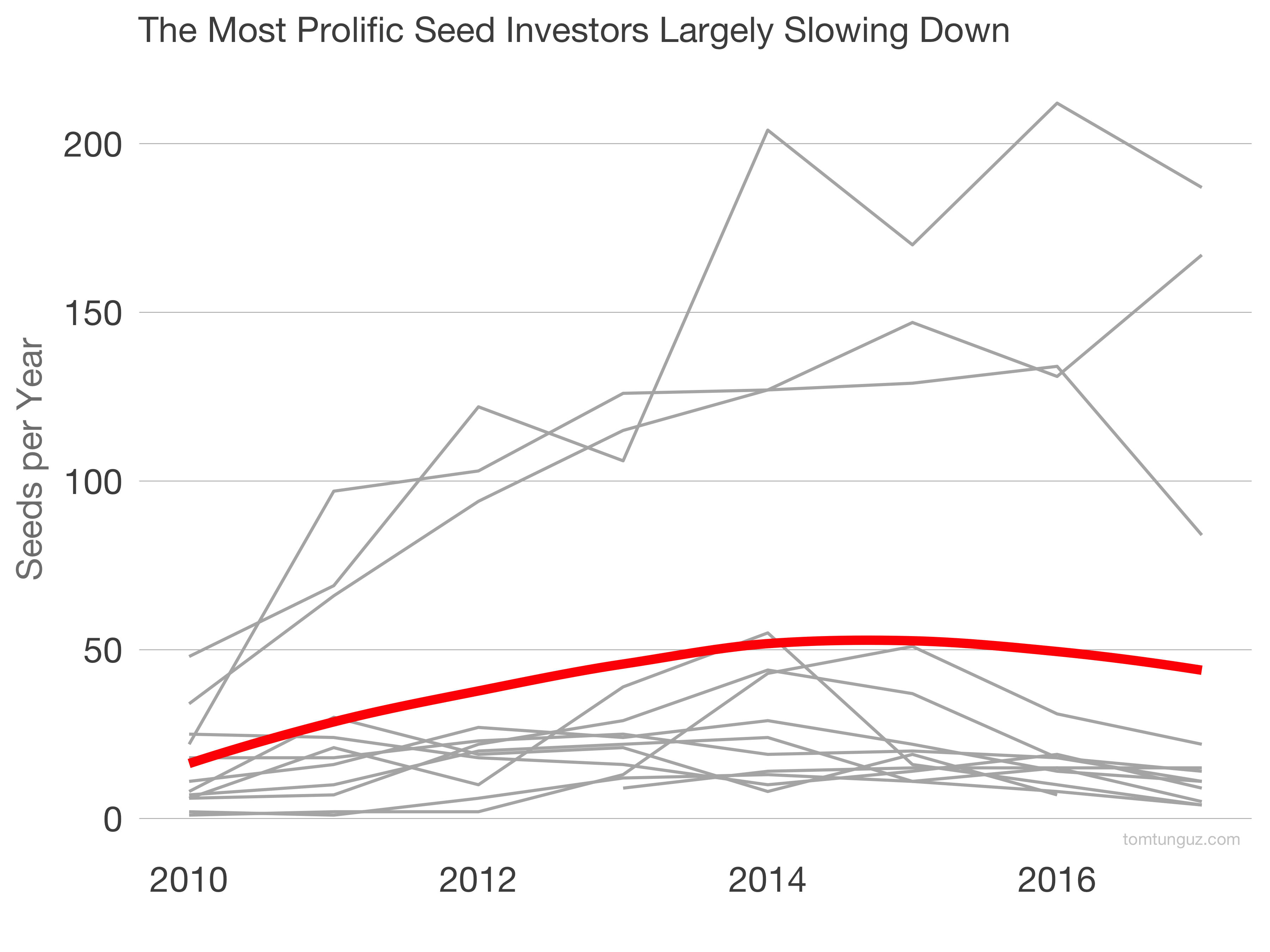

Second, many of the most active seed investors and institutional seed funds are investing in fewer companies. The largest accelerators in the US buck the trend, however. The lines in gray trace the investment counts by firm. The red sketches a smoothed aggregation.

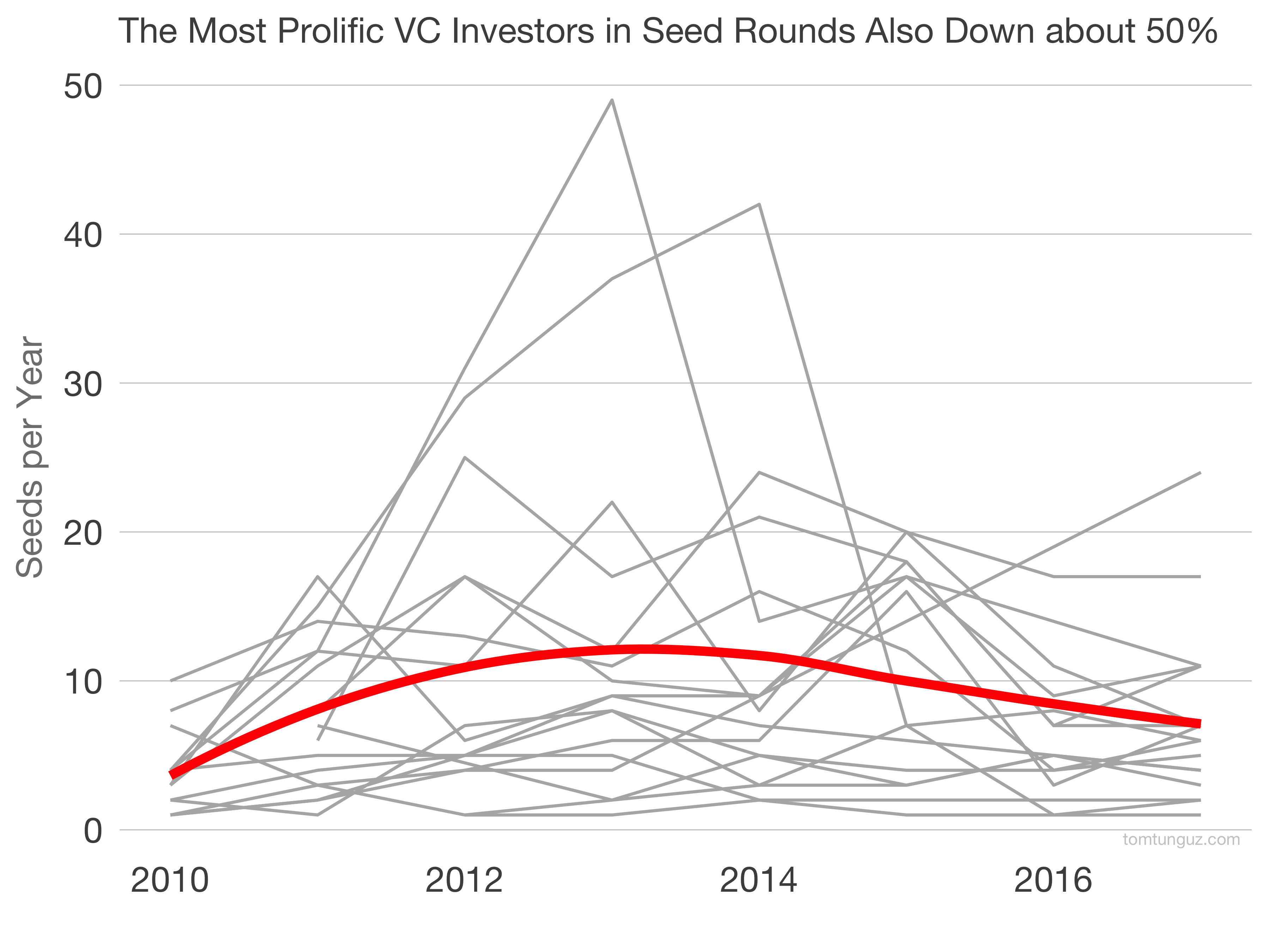

Third, all but one of the most active venture capital funds have reduced their seed investment activity. In aggregate volumes have declined by half.

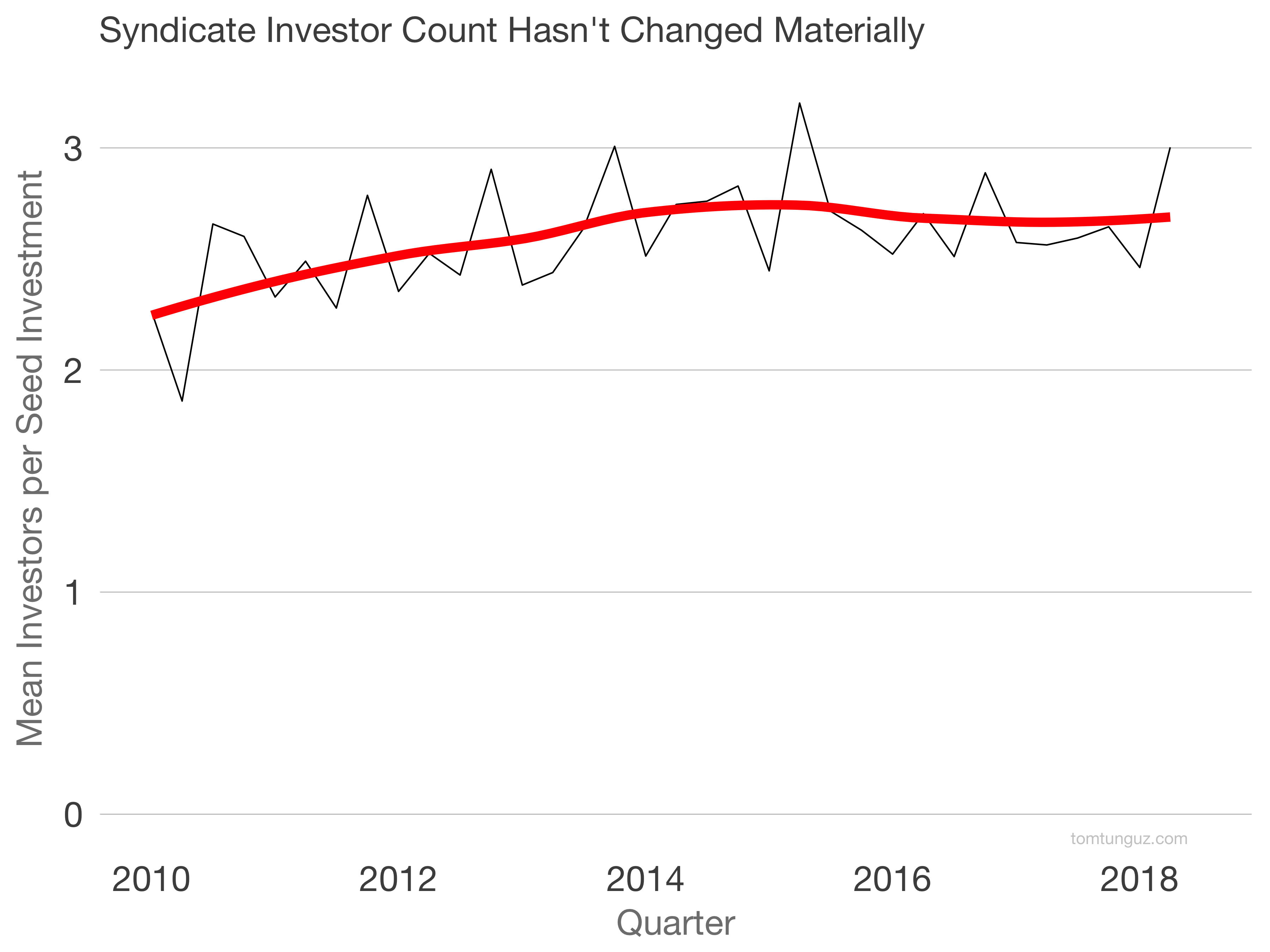

Fourth, syndicates size haven’t changed. The average number of major investors buying at the seed has remained about 2.7 investors per round throughout the gyrations of the market. And the largest party rounds have persisted of the same form, with about 20 investors.

In the midst of this, seed round sizes have tripled. Seed fund sizes haven’t tripled in the same time frame. Let’s assume they’ve remained roughly the same. If each investor deploys the same amount of capital per year, then we should expect a 2/3 reduction in seed count based solely on round size increases.

Which is very close to what we’ve seen in the market: a 62% reduction.

In summary, startup valuations have increased. This grows the size of seed rounds. Seed investors’ funds sizes haven’t kept pace, nor has VC seed investment. To buy the same ownership, investors must invest more dollars. So they invest in fewer companies and concentrate their portfolios.

What must change for the number of seed investments to increase again? More seed funds or larger seed funds must be raised, or prices must decline. The price decline can occur much more quickly than an increase in fund sizes, and that’s the more likely of the two changes. But there’s nothing on the horizon that suggests a repricing in the market today.