2 minute read / Sep 30, 2019 /

The State of the Startup IPO Market

Over the weekend, there was quite a bit of press about the challenged state of startup IPOs this year. I was curious about the real trends in share prices, so I gathered the data on some of the more salient IPOs.

The chart above shows 11 IPOs at different points in their life cycles. The leftmost column is the price of the shares at IPO, followed by the share price on the first day close, followed by Friday’s price.

There are all kinds of patterns in the data. Zoom and Pinterest have positive trajectories. The first day close is higher than the IPO price, and today’s price is higher still. You could argue that these shares were mispriced at the IPO - but that’s a topic for another post.

Companies like Uber, SmileDirectClub, Peloton and Lyft have the opposite pattern. The IPO price is the highest share price; first day close is lower; and today’s price is lower still. An interesting correlation: all of these companies are consumer businesses with lower gross margins.

A third category to see a pop after the first day of trading, followed by some compression. CrowdStrike, DataDog, Dynatrace, PagerDuty and Slack.

So, there isn’t one story here. Each company is trading differently depending on the characteristics of that business.

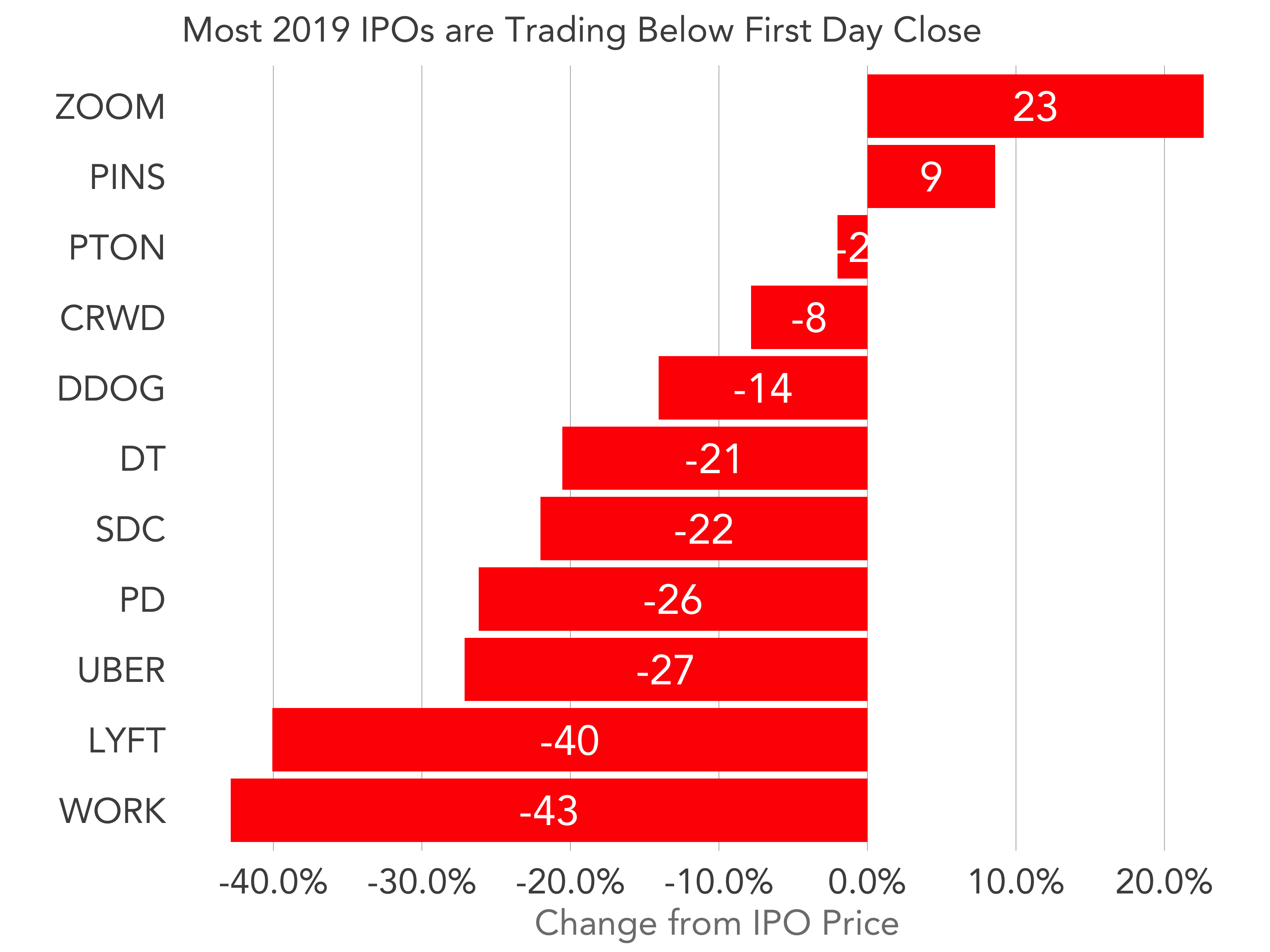

A negatively-biased story might focus on the fact that most 2019 IPOs trade below their first day close price. The chart above shows the delta between the current price of the stock and the first close price. Only two have appreciated.

A negatively-biased story might focus on the fact that most 2019 IPOs trade below their first day close price. The chart above shows the delta between the current price of the stock and the first close price. Only two have appreciated.

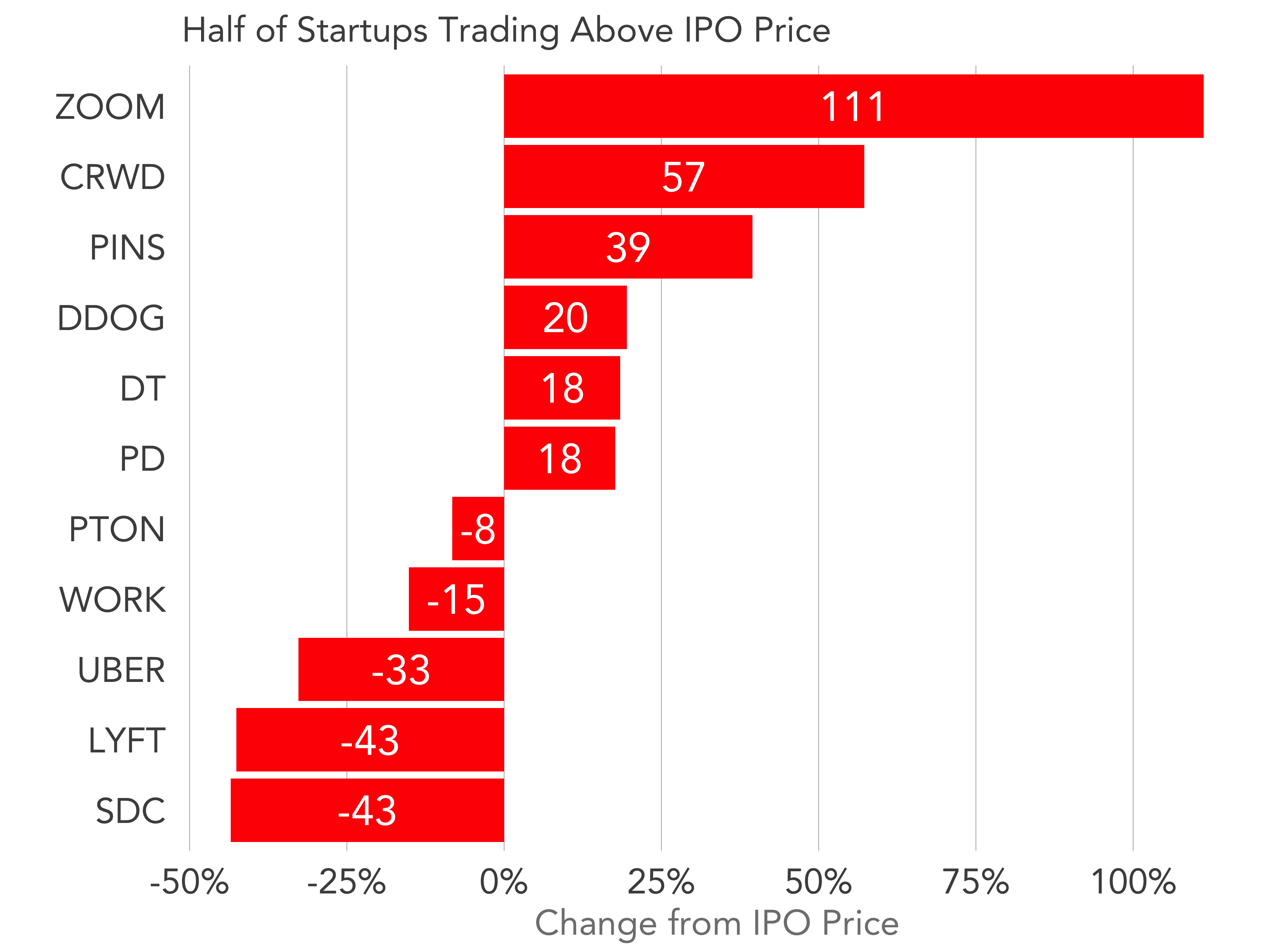

Another perspective would compare current stock prices to the IPO price, which presents a far more balanced case with about half of the names appreciating.

This data suggests that the IPO market in 2019 has been characterized by very aggressive price increases on the first day of trading, which deflate over time. This deflation may have several causes.

First, it’s hard not to cite the changing public market sentiment in the recent correction in valuations/forward multiples. Second, large holders of these shares may be selling big blocks of shares in these companies, depressing prices as lock-ups expire (or don’t exist in the case of a direct listing).

As the sentiments in the markets shift, they will impact startup valuations. And though the IPO window has been open for 2019, some of this data suggests investor demand may not be as exuberant as it was a few months ago, when growth was prized above all.