3 minute read / Sep 10, 2012 /

Profitability and the IPO Market

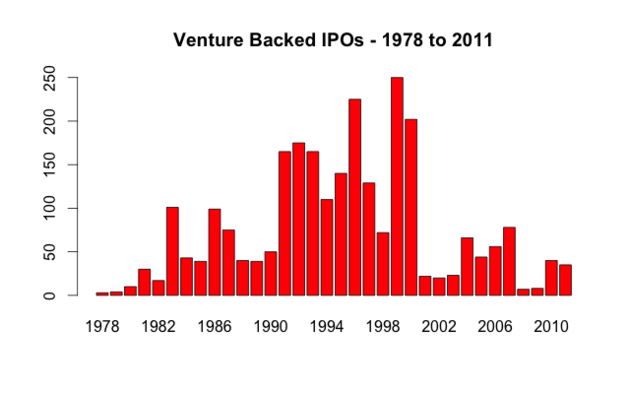

It’s a common refrain that venture backed IPOs have struggled in the past decade. For a long time, I believed and wrote supporting arguments underscoring the idea that the principal causes of this decline were Sarbanes-Oxley costs, decreasing equity coverage and decimalization of exchanges. But that’s wrong.

A paper published earlier this year uses statistics to debunk these hypotheses. In “Where have all the IPOs gone?”, a team of statisticians concludes small cap tech IPOs are struggling because today’s public candidates aren’t profitable when then file. Nor are they very profitable at all.

Small Caps Are Unprofitable and Don’t Turn the Corner

Below is a chart copied from the paper that shows the unprofitable percentage of small IPOs (those with less than $50M in trailing 12 months' revenue) and large IPOs. The fraction of small IPOs with negative EBITDA has doubled to nearly 90% in about 30 years.

| Small IPOs | Large IPOs | |||

| Number | % < 0 | Number | % < 0 | |

| 1980-1989 | 508 | 44% | 168 | 21% |

| 1990-1998 | 979 | 65% | 411 | 31% |

| 1999-2000 | 472 | 90% | 120 | 72% |

| 2001-2009 | 192 | 79% | 186 | 34% |

Once public, profits don’t improve. In the last 20 years, 80% of small cap companies hadn’t generated a profit in the first 3 years after IPO. Public investors punished them for it. Small caps share prices fell -10%.

On the other hand, large caps grew in value by 27% in the same period. 80% of these companies generated profits in the 3 years following the IPO. (See pages 38 and 39 of the paper). In short, small caps are utterly unattractive investment candidates for public market investors.

With all the talk about the decreasing costs to start a company because of the cloud and elastic computing, why are today’s small companies less profitable and ultimately far less successful in the public markets? It’s a conundrum - a secret in Thiel’s language.

Reasons for Small Cap Struggles

I don’t have the answer. But there are several theories. First, board directors are encouraging companies to remain unprofitable longer to pursue bigger outcomes. Second, the tech industry’s structure lends itself to economies of scale require small companies to operate at a significant disadvantage. Third, the decreasing costs of starting a company are increasing competition and eroding margins.

Startups may be managed differently. For example, Documentum filed for IPO in 1996 with $15M in ttm revenue and $0.5M in profit. MMC Networks filed in 1998 with $14M in ttm revenue and $0.5M in profit. We don’t see these IPOs today. Instead, venture capital growth funds are financing these companies at these stages. Perhaps these investors are encouraging companies to continue to finance growth with negative profits, a trend that continues through the public offering but ultimately, isn’t the best decision for shareholders.

The authors of the paper speculate economies of scale are to play - larger companies operate more efficient sales channels, close higher value customers and leverage distribution strength to develop near monopolies. As a result, smaller companies face greater costs in bringing products to market because of longer sales cycles and greater competition. This argument favors stronger FTC involvement in anti-trust regulation.

Lastly, perhaps, the decreasing costs of starting tech companies are creating more entrants. Without significant barriers to entry, new entrants use lower prices and freemium strategies to win market share. Such strategies ultimately reduce price points and decrease the value of a market reducing profitability for all market players.

No matter the cause, this paper does underscore the value of building a profitable business is disproportionately rewarded in the public markets for small cap companies.